Singapore’s case for energy storage starts with the grid problem it solves. The Energy Market Authority (EMA) describes Energy Storage Systems (ESS) as “giant batteries” that store excess energy for future use, and highlights that they facilitate the integration of distributed and intermittent generation into the power grid. EMA also points to ESS providing ancillary services by regulating and reserving energy, contributing to grid stability and reliability, and responding swiftly to power fluctuations. For a power system managing intermittency and peak demand, these services matter because they support reliability while enabling more variable generation to connect without destabilising operations.

Policy and market design are also part of why storage is moving into the mainstream. EMA states that ESS in Singapore can participate in the wholesale electricity market to provide services necessary to mitigate intermittency caused by solar and to reduce peak demand. It also notes the role of deployment in generating insights on performance in Singapore’s hot and humid environment, which can inform technical guidelines. On standards, EMA references SS:725-1-1:2026, an Electrical energy storage (EES) systems safety specification for grid-integrated systems. Together, market participation plus clearer safety expectations can reduce uncertainty for projects that need to connect, operate, and earn revenue.

Why BESS Momentum Is Accelerating in Singapore and Across ASEAN

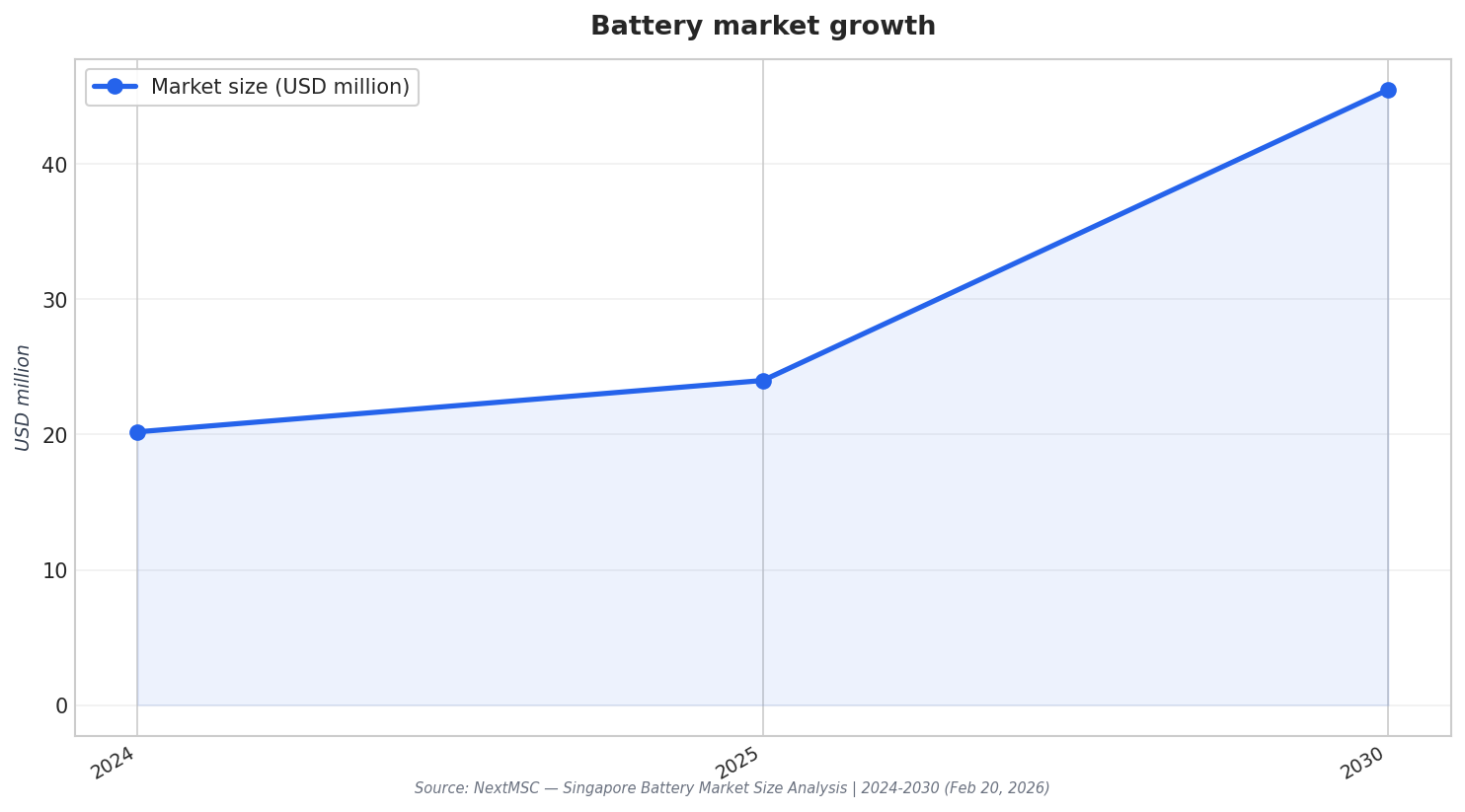

In Singapore, storage demand is tied to renewables integration and a broader battery ecosystem. Nexdigm’s market overview says Singapore’s Battery Energy Storage System (BESS) market is “valued at approximately USD ~ billion,” while emphasising the role of BESS in stabilising the grid as the country increases adoption of solar power and other renewable technologies, with government policies such as tax incentives supporting demand. A separate market view from NextMSC frames Singapore as a strategic regional hub focused on advanced battery R&D, testing, and high-value manufacturing, supported by grants and incentives for clean energy and electric mobility. It also notes that rooftop PV and floating solar projects increasingly rely on battery energy storage to manage intermittency and maintain grid stability, while industrial parks, data centres, and commercial complexes adopt batteries for peak-shaving, backup power, and energy cost optimisation.

Technology choices and use cases explain why many deployments lean toward large, grid-supporting systems. Nexdigm segments Singapore’s BESS market by technology type and states lithium-ion batteries dominate due to high energy density, longer life cycle, and decreasing costs over time, supported by established supply chains. By application, Nexdigm says utility-scale has the dominant market share because it supports grid stability and renewable integration, storing excess power during peak solar production and releasing it when demand is high or renewable output is low. In global context, Market Growth Reports says that in 2023 utility-scale storage installations represented over 70% of total market share in terms of capacity, and estimates that by 2025 over 15,000 MWh of storage capacity will be deployed globally, illustrating how central grid-facing projects are to the broader BESS story.

Regional signals reinforce why Singapore is unlikely to treat storage as optional. Mordor Intelligence projects the ASEAN energy storage market expanding from USD 3.91 billion in 2026 to USD 5.43 billion by 2031, at a 6.76% CAGR between 2026 and 2031. It adds that in 2025 pumped-storage hydroelectricity held 80.9% of storage technology demand and on-grid systems accounted for 79.1% of deployments, while grid-scale utility applications held a 47.2% share in 2025. The same report notes regional power demand rose by more than 7% in 2024 and cites APAEC 2026–2030 targets of a 30% renewable share in primary energy and 45% share in installed power capacity by 2030. For Singapore’s battery energy storage system outlook for 2026, these figures matter as context: they show a region leaning into on-grid, utility-scale balancing needs, where fast-response BESS can complement existing infrastructure and market structures.

What does Singapore’s EMA say energy storage systems do for the power grid?

How does energy storage participate in Singapore’s electricity market?

Which battery technology is described as dominant in Singapore’s BESS market?

In the Singapore battery energy storage system 2026 outlook, what kinds of sites are adopting batteries beyond the grid?

What ASEAN trends suggest storage demand is rising across the region?